Buying your first home is a momentous occasion, but the final step—closing—often comes with a list of fees that can be confusing and overwhelming.

Lowell, Massachusetts, a historic city in the Merrimack Valley, has been attracting first-time buyers looking for affordability without sacrificing culture and community.

Known as the “cradle of the American Industrial Revolution,” Lowell now offers a thriving arts scene, diverse neighborhoods, and a variety of housing options—from converted mill lofts to classic single-family homes.

This guide provides a clear breakdown of Lowell MA closing costs for first-time homebuyers, detailing what to expect, who pays what, and how to take advantage of local assistance programs that can help you get into your new home with confidence.

Understanding Massachusetts Closing Costs

Closing costs are the fees and expenses you pay at the end of the homebuying process to officially transfer ownership. These costs go beyond the purchase price and include everything from lender fees to legal services.

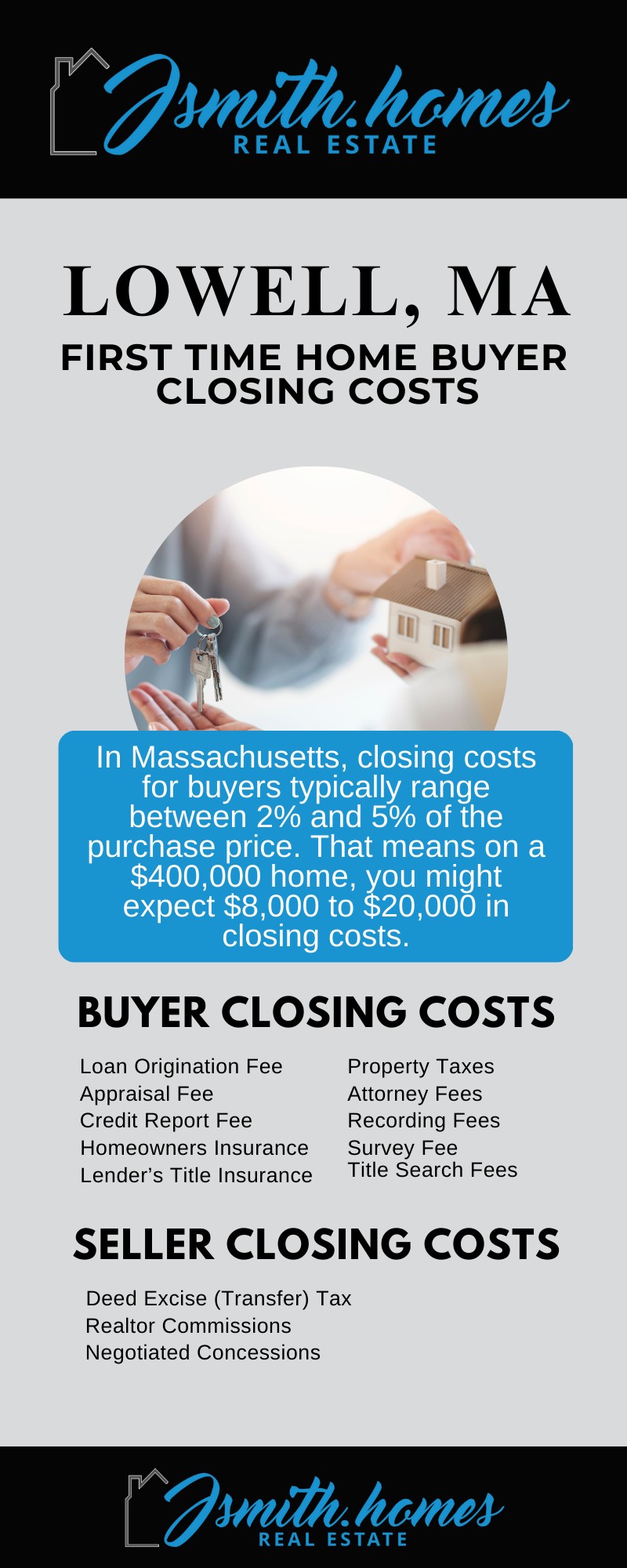

In Massachusetts, closing costs for buyers typically range between 2% and 5% of the purchase price—sometimes as low as 1.5% if you are using minimal financing. That means on a $400,000 home, you might expect $8,000 to $20,000 in closing costs.

Closing costs are a mix of:

- Loan-related fees (charged by your lender)

- Prepaid expenses (insurance, taxes, escrow reserves)

- Government and legal fees (recording, attorney, title search)

Breakdown of a First-Time Homebuyer’s Costs

Loan-Related Fees

These make up the bulk of most buyers’ closing costs.

Loan Origination Fee

Typically, 0.5% to 1% of the loan amount is paid to the lender for processing your mortgage.

Appraisal Fee

Covers a licensed appraiser’s report on the home’s value; expect $500 to $1,000+.

Credit Report Fee

A small fee (usually under $50) to pull your credit history.

Lender’s Title Insurance

Protects the lender from title disputes; this is required for most mortgages.

Prepaid Expenses

These are upfront Lowell, MA, closing fees collected to set up your escrow account.

Homeowners Insurance

Your first year’s premium is typically paid at closing.

Property Taxes

A prorated share for the remainder of the year, plus a reserve for upcoming payments.

Government & Legal Fees

Attorney Fees

In Massachusetts, hiring a real estate attorney is standard practice. Fees range from $800 to $1,800 depending on complexity.

Recording Fees

Paid to the Middlesex North Registry of Deeds to officially record your deed and mortgage.

Survey Fee

Sometimes required by Lowell, MA, mortgage lenders to confirm property boundaries.

Title Search Fees

Ensures no liens, unpaid taxes, or other claims exist on the property.

The Role of the Seller

Deed Excise (Transfer) Tax

In Massachusetts, sellers typically pay the deed excise tax—$2.28 per $500 of property value. For a $400,000 home, that’s about $1,824.

Realtor Commissions

While technically not a closing cost for the buyer, sellers usually pay the real estate agent commissions (5% to 6% of the sale price).

Negotiated Concessions

If the market favors buyers, you may be able to negotiate for the seller to cover some of your closing costs, which can be a huge help for first-time buyers.

Special Programs for First-Time Buyers in Lowell, MA

City of Lowell HOME Program

This federally funded program offers up to $11,800 as a no-interest loan for eligible first-time buyers. The funds can be applied toward your down payment and closing costs.

Homebuyer Education

To qualify for most assistance programs, you’ll need to complete an approved homebuyer education course and receive a certificate of completion.

Other Assistance

Local credit unions offer grants and programs that can further reduce your out-of-pocket costs, so be sure to explore these options early.

Tips for a Successful Closing

Plan ahead for closing costs of 2% to 5% of the purchase price. Setting aside these funds early avoids last-minute surprises.

Many programs require a home inspection before closing. Even if not required, this is a vital step to uncover any major issues before you commit.

If you’re using Lowell’s HOME Program, expect about three weeks for processing after submitting a complete application—factor this into your closing schedule.

A local real estate agent, a mortgage broker familiar with first-time buyer programs, and a Lowell-based attorney can help you avoid delays and keep the process smooth.

Conclusion

Closing costs can seem daunting, but with the right preparation, they don’t have to stand in the way of homeownership. We’ve broken down the key expenses, explained the seller’s role, and highlighted the assistance programs available in Lowell.

With proper planning, trusted local professionals, and possible financial help through the City of Lowell’s programs, buying your first home here can be a realistic and rewarding goal.

Ready to take the next step? Connect with a local real estate agent, get pre-approved, and start your journey toward homeownership in Lowell today!

Frequently Asked Questions

What is the average amount for closing costs in Lowell, MA?

Typically 2–5% of the purchase price, depending on your loan and lender fees.

Are there down payment assistance programs in Lowell for first-time buyers?

Yes—the City of Lowell HOME Program offers up to $11,800 in assistance, and other local lenders may offer grants.

What is the role of an attorney in a Massachusetts real estate closing?

Your attorney will review contracts, clear the title, and represent your interests at the closing table.

Who pays the transfer tax in Massachusetts?

The seller customarily pays the deed excise tax.

How much of a down payment is typically needed for a home in Lowell?

While 20% is traditional, many first-time buyer programs and loans allow as little as 3–5% down.

What documents are required for a first-time homebuyer program?

Typically, proof of income, bank statements, tax returns, and a certificate of completion from a homebuyer education class.

How does the home inspection process work in Lowell?

You hire a licensed inspector who examines the home’s systems and structure. The report helps you decide whether to move forward or renegotiate with the seller.